Until I met J, I wasn’t very good with saving money on anything. I used to stick to the same companies year on year for my insurance, mobile and internet providers because I was too lazy to switch. I’d also buy the same products all the time, not even looking at whether there was a cheaper alternative.

I’m now completely reformed and consider myself to be pretty savvy, so I thought I’d thought I’d share some of the tips I’ve learnt!

Whether you own your own place or you’re renting, home insurance is pretty essential, just in case things don’t go to plan. If you’re renting, you only need contents insurance but if you’re a homeowner then buildings and contents is the one for you; most mortgage providers will need you to do this as part of your agreement.

First things first:

- Never ever just accept the renewal quote from your current provider, it will almost certainly be higher than any quote you can find yourself. It might be boring and time-consuming, but looking around could save you around £40 or more!

- I set a reminder on my phone a good couple of weeks before my renewal is due as, once it starts getting closer to that date, the prices will generally go up!

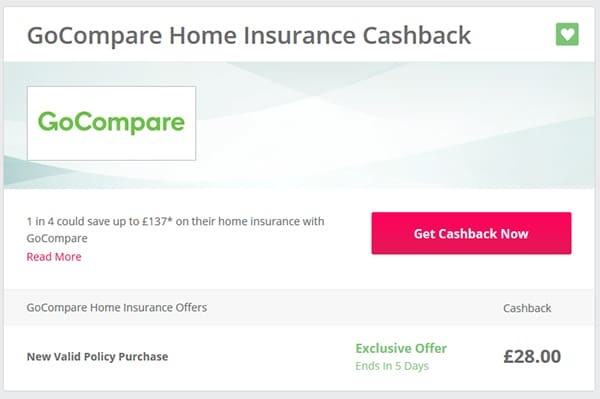

- One of the best ways I’ve found to save money on our home insurance is going through Topcashback* (TCB); the UK’s highest paying cash back site. I start by checking out two of the big comparison sites; Go Compare and Compare The Market. The cashback offered varies depending on the day. Unfortunately, Money Supermarket isn’t available on TCB.

How Topcashback works:

- I pick the comparison site I want to check out (obvs starting with the one with the highest cash back, in this case, Go Compare) I then click “get cashback now” and it will take me directly to the comparison site, while recording my visit on TCB.

- Once I’ve added all my details in, it will show you all the quotes from cheapest to most expensive. Just so you know, unless it’s clearly stated, the cash back isn’t usually included so you can deduct the amount of cash back from the prices. For example, if a quote is £100, and cash back is £28, the quote will actually be £72.

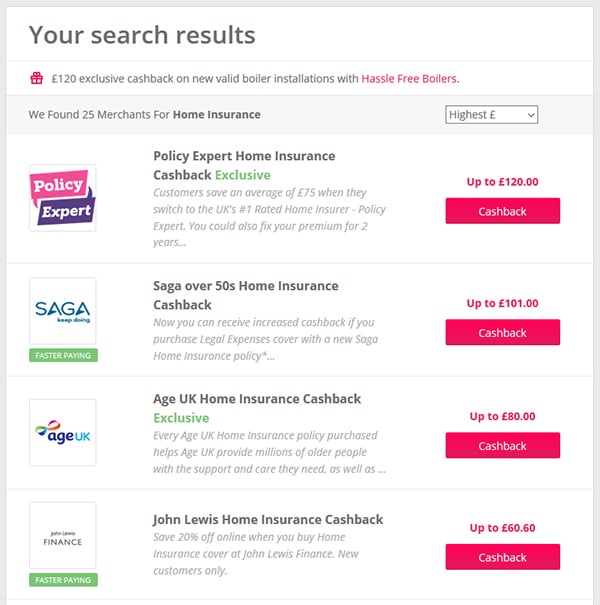

- After I’ve checked the comparison sites, I also check independent providers on TCB as well by searching for “home insurance” in the search bar and then changing the order to highest £ (this means it’s ordered by the highest amount of cash back to the lowest). Some of these look like they can offer massive savings, although be aware that the quotes are generally higher! I only tend to check the first 4 or 5 to make sure I really am getting the best deal as the quotes are often ridiculous; one company was quoting us £274!!

The finer details:

- Sometimes your job description can cause the price to go up and down. For example I’m a medical secretary but I guess I could also be described as an admin assistant. I’ve found that putting secretary will generally get a slightly cheaper quote than putting admin assistant so it’s worth checking if you could word your job in an alternative way. Don’t out-and-out lie though as that will invalidate any claim you make.

- Some companies will give a higher rate of cash back for combined insurance policies (building and contents) but if you can be bothered, you could try getting quote for separate policies to see if it gets you more cash back.

- It’s also worth playing around with the voluntary excess figures, as sometimes having the highest amount (usually £500) will only make your quote a few pounds less than if you dropped the excess to £350 or £200, which in the long-run, will save you money if you do need to claim.

- Contents insurance is a tricky one as it’s bloody time consuming working out what stuff you have and how much it would cost to replace it as new and, if you underestimate and need to claim, you might end up losing out big time. Luckily a few of the companies auto-suggest that £35,000 is around the UK average but you might find they say that you can claim up to £75,000.

- Paying annually and not monthly, if possible, will also bring your amount down.

Terms and conditions:

- If you’ve had a policy with a company before, it might invalidate your cash back. For example, Policy Expert are currently offering a massive saving on home insurance, but as they were our provider a couple of years ago, we wouldn’t be eligible to claim the cash back.

- If you decide to get a quote and don’t go through with it, starting again a few days later might not register with Topcashback and you could miss out on your cash back. To combat this, either open TCB up in a private window or delete your cookies. You also can’t use a previously saved quote so if you come back to it later on, you will have to fill out the forms again. Oh the fun!!

- The other thing worth remembering is that, if you cancel you claim within 3 months of it being active, you won’t earn any cash back.

And finally:

- Once you have a quote you’re happy with, you can always ring your provider and say this is what you’ve found, could they match it?

- If you they can’t match it and you are going to change your provider, check whether you’re on an automatic renewal or not; it should usually say on your renewal paperwork/email!! If you are set up for auto renewal, they’ll take the money out of your account on your renewal date so you must remember to call to say you won’t be renewing with them.

How do you save money with your home insurance? Let me know in the comments below 🙂 x

*Disclaimer: This isn’t a sponsored post, I just love TCB but, if you choose to sign up to it using my link, I’ll get a £5 reward when you’ve earnt £5.

5 Comments

Wow! I have never really understood how these sites work but this is interesting! I’ll deffo be looking into this in the future! Thanks for sharing xx

They’re one of my favourite things, I think I’ve earnt about £125 in the last few months! xx

Wow!!

Yep, there are so many things you can use it for; including shopping!! Asos is on there if I remember correctly which is pretty useful 😀 x

I’ll be checking this out today. 🙌🏼🙌🏼